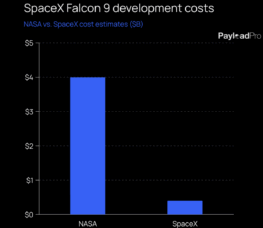

Falcon 9: SpaceX vs. NASA Costs

Look at all those savings.

But there are enormous technical hurdles that need to be overcome. So, we spoke to Starcloud and Sophia Space, two startups building data centers in space, to understand the opportunity and separate the fact vs. fiction.

The Israel-Iran conflict has extended to space with exo-atmospheric interceptors, satellites providing critical comms, and remote sensing spacecraft beaming down images for intelligence gathering.

Amid the NASA budget bloodbath, the Commercial LEO Destinations program has emerged still standing.

Florida’s Space Coast continues to dominate US launches, but Vandenberg is the fastest-growing launch site.

SpaceX launched 16 Falcon missions in May, tying a monthly record for the workhorse rocket.

NASA has paid out $2.6B of SpaceX’s Human Landing System (HLS) contract, representing 65% of the $4B current award amount and 58% of the $4.5B potential award amount.