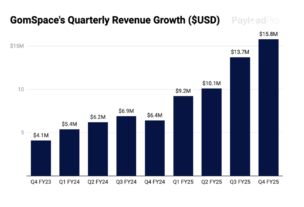

GomSpace Revenue

There’s a reason why Danish smallsat manufacturer GomSpace’s stock is up 400% over the last 12 months.

There’s a reason why Danish smallsat manufacturer GomSpace’s stock is up 400% over the last 12 months.

The investor playbook has flipped: In the era of AI, Asset-light, high-margin good businesses (software) start to look bad, while greasy, capital-intensive, bad businesses (hardware) now look good. That’s just as true in space as anywhere else.

Space businesses continue their burn streak.

Another space business is hitting public markets.

We forecast that SpaceX’s revenue will increase from $15B in 2025 to $23.8B in 2026, driven by Starlink’s customer base doubling from 9.2M to 18.4M.

Payload is back with our 2025 SpaceX revenue model build.

2025 was the year of a convergence of tailwinds in the space industry.

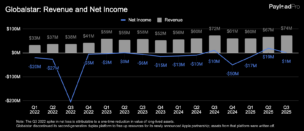

Globalstar’s future is inextricably tied to Apple—not a bad position to be in.