Our Launch Cadence Forecast For Next-Gen Rockets

What should we expect the flight cadence ramp to be for next-gen reusable rockets like New Glenn, Neutron, Nova, Terran R, and Eclipse?

What should we expect the flight cadence ramp to be for next-gen reusable rockets like New Glenn, Neutron, Nova, Terran R, and Eclipse?

Hundreds of space companies we have all grown to know and love were founded—and raised billions of dollars—on the assumption that SpaceX had solved launch with Falcon 9, all but guaranteeing reliable, predictable access to orbit. But that premise is now on shaky grounds, turning the future of many satellite businesses into an existential question.

The FCC’s latest processing round has attracted proposals spanning nearly 140,000 satellites from 13 constellations, kicking off the next battle for valuable satellite spectrum. While many of these constellations may never launch, the filing deadline determines who gains a critical regulatory advantage for years to come.

For many satellite applications, optical links are not worth their cost (often hundreds of thousands of dollars).

We cover terrestrial bottlenecks, cost analysis, the competitive landscape, and technical challenges.

The technical challenges to orbital data centers are well understood, and boil down to the following:

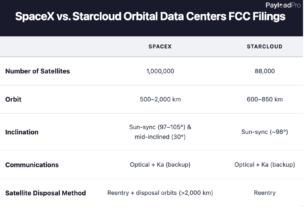

After only a two months of 2026, this year is already shaping up to be the year of space data centers. In January, SpaceX filed with the FCC for up to 1M satellites (wild). A few days later, Starcloud followed with plans for 88,000 satellites of its own.

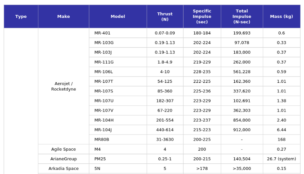

A catalogue of in-space propulsion options—vendors, products, and specs.

Earlier this week, Kepler (an optical comms relay business) launched its first ten 300-kg sats and announced a deal with OroraTech, to host its thermal sensors and speed up downlink via its laser-linked routing.

Some of that spectrum still sits in legacy hands, ripe for acquisition.